SpaceX went public on June 12 under the ticker SPCX, and the first two and a half weeks have been a roller coaster: an open near $150, a close near $161 on day one, an all-time high of $225.64 on June 16, and an all-time low of $147.11 on June 23. As of June 29 the stock is trading around $156. The more interesting number is what the options market is quoting for where it could be a month, a year, and two years out, and those numbers are big.

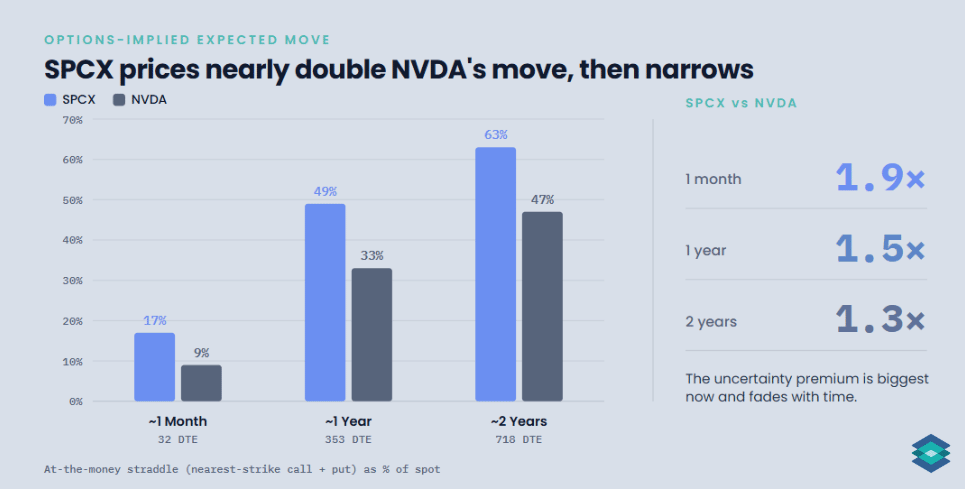

For most of my career as an options broker I was constantly watching implied volatility and expected moves across hundreds of names. You develop a feel for what normal looks like at each expiration. SPCX stuck out. The premium on this chain runs well above what I am used to seeing on a stock this liquid. For context I pulled NVDA, a stock everyone accepts is volatile, for the same expirations. It isn't close. A month out, SPCX prices nearly twice the move the market wants on NVDA, and stays richer all the way out to two years. This is a brand-new listing, and the chain is telling you the market has very little settled about it.

The expected move, three ways

The cleanest way to read what the market expects is the at-the-money straddle: buy the call and the put at the strike nearest the stock price, add up what you pay, and that is roughly the move the stock has to make by expiration to break even. It is the price of the expected move, in dollars you would actually spend.

For SPCX, currently trading at $156:

The ~1 month expiration (32 days out) prints an at-the-money straddle of about $26.50, the 155 call plus the 155 put. That is roughly 17% of the stock's value in a single month. A buyer needs the stock to move more than $26.50 in either direction to break even. Note this expiration lands in late July, just before the company's first earnings report on August 6, so the biggest known catalyst sits just outside this window.

The ~1 year expiration (353 days out) prints a straddle of about $77, or roughly 49% of spot. The market is not expressing a view on direction here. It is saying the range of plausible outcomes a year out is very wide, wide enough that a near-50% round trip in either direction is on the table.

The ~2 year expiration (718 days out) prints a straddle of about $99, or roughly 63% of spot. That is a large number, but worth being precise about. It does not say the stock is a coin flip between zero and double. It says owning both sides of this name for two years costs you nearly two-thirds of the share price, which is what happens when you stretch a 60%-plus implied volatility across that much time. The takeaway is the width itself: a low-confidence view of where this lands two years out.